Business bank accounts for sole traders

Separating personal and business finances is essential when running your own freelance business. Choosing the right sole trader business bank account streamlines operations and simplifies tax time.

Article contents

− +

When you’re running your own business, finances can become very complex. A dedicated business bank account makes it much easier to stay organised and prepare for tax season.

In this guide, we’ll walk through:

Essential bank account types for sole traders

Criteria for choosing the best business bank account

Strategies for managing your money across accounts

What bank accounts do sole traders need?

If you’re like many people, you’ve probably only had two bank accounts up to now: a personal account and a savings account. But as a freelancer, you will need to set up a couple of new bank accounts to make sure your money always lands in the right place.

Business transaction account

This is the account you will use to accept payments from clients. It functions just like a normal transaction account, except the bank and the Australian Tax Office (ATO) will see that it’s associated with your business, which is important when you file taxes.

You will also use this account for any business expenses you may have, including software, supplies, or office space rentals. Mixed expenses used for both business and personal reasons such as phone or utility bills should also be paid from this account. We’ll show you how to parcel these out appropriately later on in the article.

Business savings account

This account isn’t required but is sometimes included at no cost when you set up a business transaction account. (It’s useful having an extra account, so it’s worth shopping around to find a bank account that includes a free savings account.)

It’s not a bad idea to use this account as an emergency fund—if you have unexpected business costs, you can withdraw some money from your business savings into your business transaction account to cover it.

You can also use your business savings account to store money you’ve set aside to pay your freelance taxes. Business savings accounts usually earn interest (provided you keep a minimum amount in the account), so if you have money that you will be holding on to for a long time, it pays—quite literally—to keep it stored in this account.

What about business credit cards?

When setting up your business bank accounts, you'll likely encounter offers for business credit cards. These cards function similarly to personal credit cards but are designed for business expenses, often with rewards programs tailored to business spending.

Banks pitching these cards often highlight benefits like building business credit and accessing higher credit limits. But while these perks can be attractive, approach business credit cards with caution.

As a sole trader, you're personally responsible for any business debt incurred, and the high interest rates can quickly become a burden if not managed properly.

Only consider a business credit card if you have a solid plan for managing and paying off the balance regularly, and if the benefits clearly outweigh the potential risks for your specific business needs. Many successful sole traders operate without credit cards, especially in the early stages of their business.

If you're unsure, it's often safer to stick with a debit card linked to your business transaction account until you're more established and have a clear need for credit.

How to find the right business bank account for you

It’s relatively easy to set up a business bank account, but choosing the right bank can be tricky because there are so many options.

The first big question: Should you go for one of the big four banks (Westpac, ANZ, NAB, and Commonwealth), or should you branch out and try a different bank?

If you are already using a bank for your personal accounts, the easiest option may be to set up your business bank accounts with the same institution. This will make it easier for you to transfer finances as needed from one account to another, without too much hassle.

If you’re looking to find a new bank for your business accounts, you could consider one of the newer banks that have popped up in recent years, many of which are exclusively online, including Up Bank or 86 400.

Ultimately, it comes down mostly to personal preference, as most banks offer the different types of accounts you need. Consider how important it is to be able to go into a physical bank—if that’s something you value, then avoid choosing an online-only bank.

The best bet when looking for a new bank is to use tools like Finder or Canstar, which let you compare business bank accounts side by side.

What are the monthly fees and ATM charges?

Banks offer different fee structures for business accounts. Some may charge a flat monthly fee, while others waive fees if you maintain a minimum balance. ATM fees can add up quickly, especially if you frequently need cash for your business. Look for accounts that offer fee-free ATM access or a wide network of no-fee ATMs.

How functional is their digital banking platform?

Most banking is done through a computer or mobile device, so you want to choose a banking platform that serves your freelance business needs. Look for features like real-time transaction updates, easy fund transfers, bill pay services, and mobile check deposits. A user-friendly interface can save you time and make managing your finances on-the-go much easier.

Do they participate in Open Banking?

Banks participating in the Open Banking initiative allow you to securely share your financial data with third-party services, including accounting software like Rounded. All major banks (and many smaller banks) in Australia are part of this initiative, but if you want to be certain, you can search for your bank on the Consumer Data Right database.

Do they offer any perks and bonuses?

Some banks offer perks to attract new business customers. These might include cash bonuses for opening an account, cash back on certain types of purchases, or higher interest rates on savings. While these shouldn't be the primary factor in your decision, they can be a nice added benefit if all other features meet your needs.

How well does this bank operate overseas?

If you plan to work with overseas clients or become a digital nomad, consider a bank with favourable international transaction fees and exchange rates. Some banks offer multi-currency accounts or partnerships with international banks, which can be valuable for global business operations.

Does it come with a linked savings account?

Many banks offer a free business savings account when you open a transaction account. This can be useful for setting aside money for taxes or building an emergency fund. Look for accounts with competitive interest rates and no or low minimum balance requirements.

Will you receive a debit card?

Check if the account comes with a debit card for business purchases. This can help you keep personal and business expenses separate and may offer additional benefits like purchase protection or extended warranties on business-related purchases.

It’s up to you to decide how important these questions are for you, but this should help you narrow down the list and find the best option.

After that’s done, it’s quite simple to set up a business bank account. This can often be done online in just a few clicks, but if you prefer, you can visit a nearby branch and go through the setup process with a bank employee.

How to manage your money in your new bank accounts

Now that you’ve gone through the process of setting up the accounts, you’ll find it’s much easier to keep your cash flow and expenses in order. Here’s a quick guide on how to sort your finances going forward:

1. Payments come into your business bank account

Any time you get paid by a client or customer, the funds should go directly into your business bank account. If you use Rounded to send custom invoices, it’s very simple to update your banking information so that payments come directly into the right account.

2. Set aside taxes in your business savings account

As a sole trader, you most likely pay quarterly taxes. This means you need to be proactive, setting aside the right amount of money every time you get paid, so that you don’t accidentally spend it. If you know which income bracket you fall into, you can easily figure out a quick formula to transfer a certain percentage of your wages for safe keeping.

Here’s a tip from Lauren Thiel, a certified accountant and owner of The Real Thiel: "Have a bank account specifically for tax. I nickname mine 'not my money'. Put a little aside every week, and then when you get to the end of the year, or to your quarterly activity statements, you have the money there ready to pay to the ATO. This should relieve a lot of the financial stress around tax time because you are prepared in advance.”

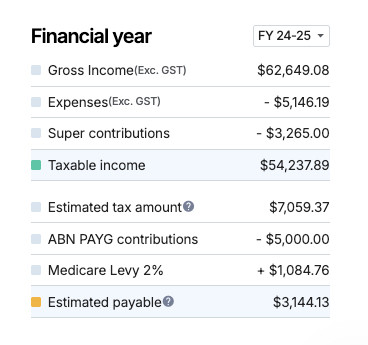

If you’re a Rounded customer, you’ll see an estimate of your income tax liability on the dashboard, which updates as you add your income and expenses. This estimate is based on the data you enter into your Rounded account, so it’s always a good idea to check the number with your accountant or the ATO.

Rounded automatically estimates how much tax you need to put aside based on the data you add

3. Only make business purchases using your business account

Get in the habit of only using your business account to pay for things that are legitimate business expenses. This will make your life a lot easier when it comes time to file taxes because you’ll know that anything taken out of that account is tax deductible. Be sure you change any automatic bill payments or subscriptions you use for your business to the correct account.

4. Connect your business account to accounting software

Rounded users can connect their business bank account directly to the platform, making it much simpler to organise your business expenses.

Once your account is connected to Rounded, you can easily go through and see all of your business transactions in one place.

Rounded’s AI-powered expense tracker automates the process using your past transaction history. It will determine the vendor, GST expense, status, category, and even the percentage that counts as a business expense. All you need to do is review and approve it, and you’ll be prepped for tax time.

5. Pay yourself into your personal account.

Now comes the fun part—paying yourself! Once you have set aside money for business expenses and tax deductions, you know that the rest of the money is yours to keep. Simply transfer your remaining funds into your non-business transaction account, and you can rest easy knowing that all of those funds are yours to use as you see fit.

Using your bank account for long-term financial planning

Your sole trader bank account is a powerful tool for financial planning.

Regularly analysing your spending and income streams helps you gain a deeper understanding of your business. The data can reveal areas where you might be able to save money or reduce your tax bill by shifting your spending.

Many banks include budgeting and reporting functions within their app, allowing you to categorise expenses or set spending limits.

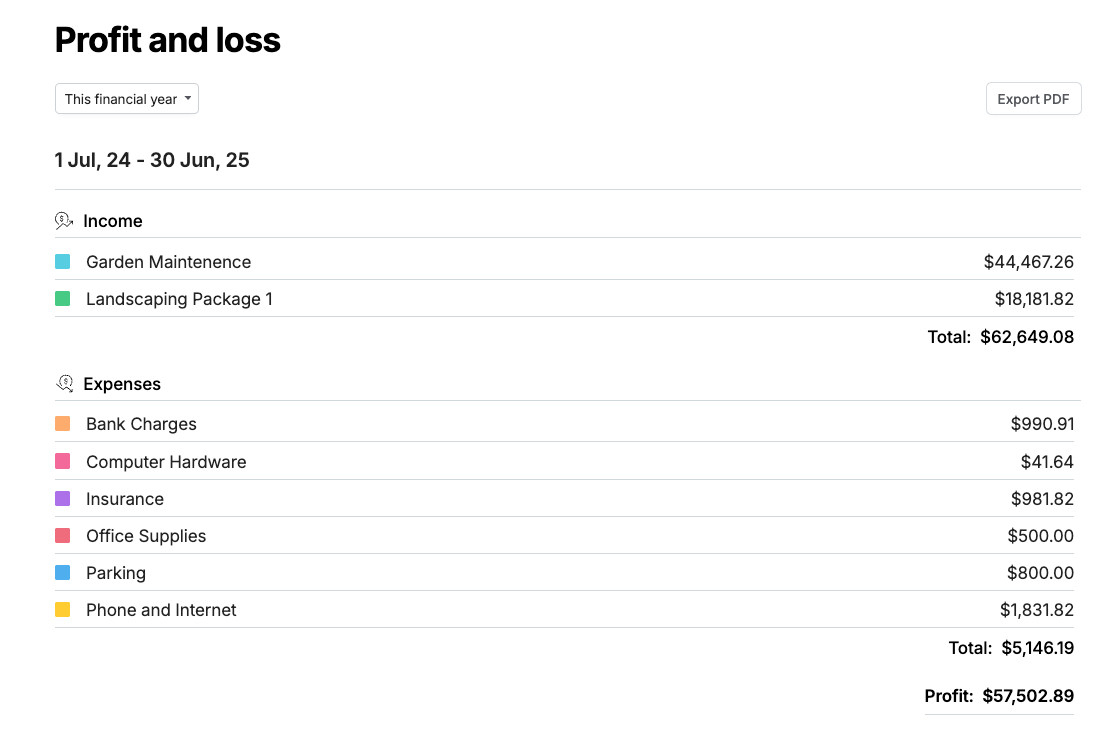

If you’re already a Rounded user, you can generate profit and loss reports directly from your dashboard, which gives clear visualisation of financial trends within your business.

For non-rounded users, there are third-party apps like Frollo and WeMoney that offer similar budgeting and reporting features.

Learning how to use your business accounts as a freelancer takes a little bit of work at the start, but once you’ve figured out a routine, it’s smooth sailing. Getting it sorted out now means you’ll have less to worry about once tax time arrives.

Looking for more advice on how to manage your freelancer finances? Check out our Freelance Advice Library.

Not using Rounded yet? Sign up for a free trial.

Cover Photo by Eduardo Soares on Unsplash

Contents

Join newsletter

ABOUT ROUNDED

Invoicing and accounting software for sole traders. Get paid faster and relax at tax time.

-p-1600.jpeg)